How to Navigate the HSA vs. FSA Dilemma

What Seas Are Surrounding Spain

September 14, 2023

How to Win Big in the Real Estate Game: Pro Tips

September 17, 2023

Healthcare expenses are a significant part of our lives, and it’s essential to make informed decisions about how to manage them. One common decision individuals face is choosing between a Health Savings Account (HSA) and a Flexible Spending Account (FSA). In this article, we will demystify the HSA vs. FSA dilemma and help you make the right choice for your healthcare needs.

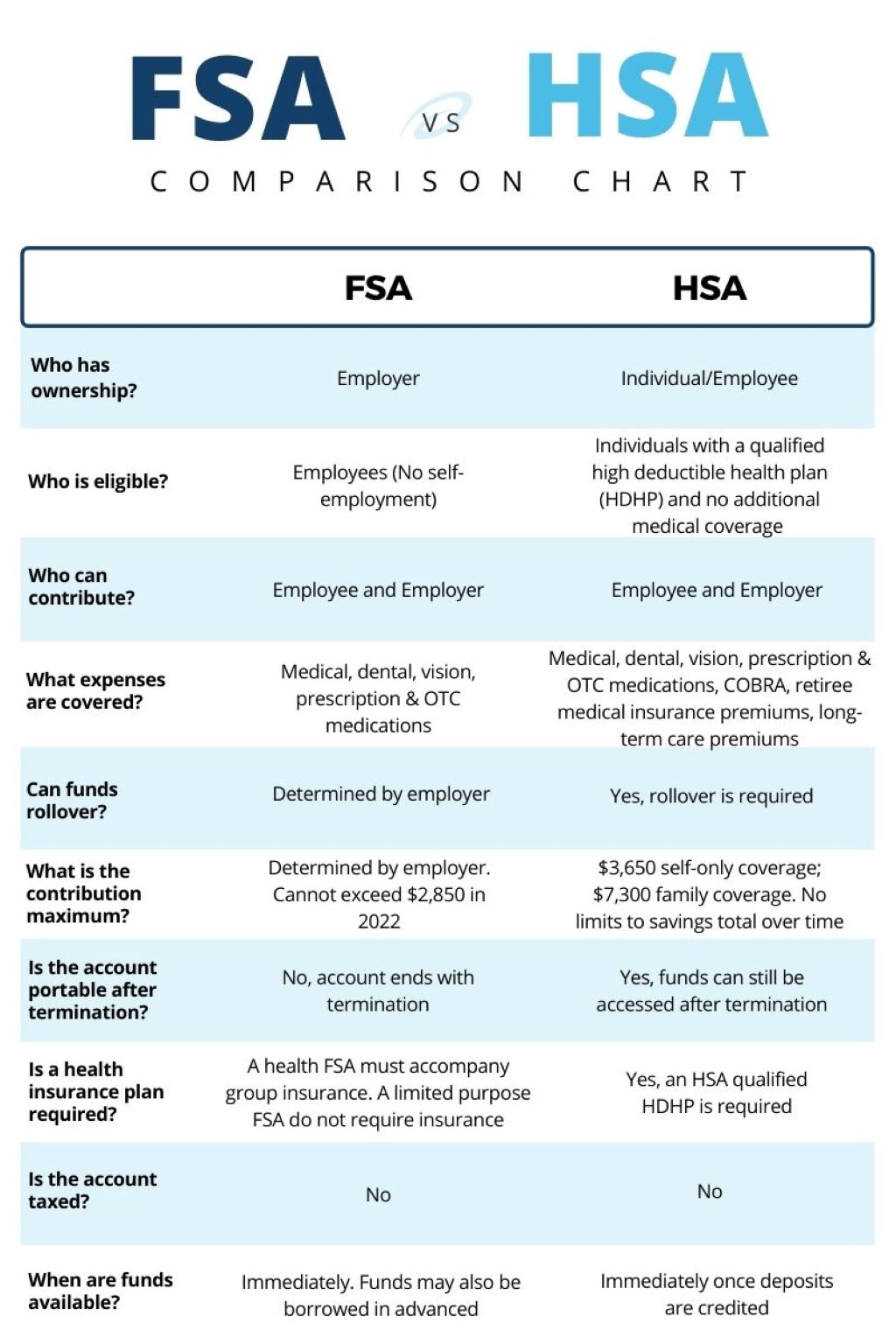

Understanding the Basics

HSA: Your Financial Ally

Have i accidentally used my hsa card for groceries? No need to fret, it’s a common mistake. HSAs are a tax-advantaged way to save money for medical expenses. It’s like having a savings account with extra perks.

FSA: The Flexible Option

Flexible Spending Accounts (FSAs) also help you save on taxes, but they come with a twist. You need to use the funds within a specific timeframe, typically the calendar year. It’s a “use it or lose it” situation.

Qualification Criteria

HSA Eligibility

To open an HSA, you must have a High Deductible Health Plan (HDHP). This plan often has a lower monthly premium but higher out-of-pocket costs when you receive medical care.

FSA Availability

FSAs are more accessible as many employers offer them, regardless of your health plan. However, there are annual contribution limits.

Contributions and Limits

HSA Contributions

HSAs allow you to contribute a substantial amount each year, and the limit tends to increase annually. This money is yours to keep, even if you change jobs.

FSA Limits

FSAs have a lower contribution limit compared to HSAs. However, they can still help you save on taxes and manage your healthcare expenses efficiently.

Tax Benefits

Tax Advantages of HSAs

HSAs offer triple tax benefits. Your contributions are tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses are also tax-free.

Tax Benefits of FSAs

FSAs provide tax advantages, but they are not as comprehensive as HSAs. Your contributions are pre-tax, reducing your taxable income.

Investment Opportunities

HSA Investment Potential

One of the unique features of HSAs is the opportunity to invest your funds in various financial instruments, such as stocks and bonds. Over time, this can significantly boost your healthcare savings.

FSA Investment Options

FSAs do not typically offer investment options. The money you contribute is meant for immediate healthcare expenses.

Portability

HSA Portability

HSAs are portable, meaning you can take them with you even if you change jobs or health insurance plans. This flexibility can provide peace of mind.

FSA Limitations

FSAs are generally tied to your employer, and you may lose the funds if you switch jobs.

Decision-Making Process

Assessing Your Health Needs

Consider your current health status and potential future medical expenses. HSAs are excellent for long-term savings, while FSAs are more suitable for immediate needs.

Evaluating Your Financial Situation

Review your budget and assess how much you can comfortably contribute. Both accounts can help you save, but you must find the right balance.

Consulting a Financial Advisor

If you’re still uncertain about the HSA vs. FSA choice, it’s a wise idea to seek advice from a financial advisor who can provide personalized guidance.

Conclusion

In the HSA vs. FSA dilemma, there is no one-size-fits-all solution. Your decision should align with your unique healthcare needs, financial situation, and long-term goals. When considering how a business can save on costs, it’s crucial to explore practical strategies such as HSAs’ tax advantages and investment potential, alongside FSAs’ flexibility for immediate expenses; taking the time to evaluate your circumstances and seeking expert advice can help make an informed choice.

FAQs

- Can I have both an HSA and an FSA at the same time?

- Yes, but there are restrictions. You can have both if your FSA is a Limited-Purpose FSA, which covers only dental and vision expenses.

- What happens to my HSA or FSA if I change jobs?

- Your HSA is portable and remains with you. However, your FSA is tied to your employer, so you may lose unused funds if you switch jobs.

- Are over-the-counter medications eligible for reimbursement with HSA or FSA funds?

- Yes, many over-the-counter medications are eligible for reimbursement, but you should check the specific guidelines for your account.

- Can I use HSA or FSA funds for cosmetic procedures?

- Generally, no. Cosmetic procedures are usually not considered qualified medical expenses.

- Is there an age limit for contributing to an HSA?

- No, there is no age limit for HSA contributions as long as you have an eligible High Deductible Health Plan.

{kind=link}

{kind=link}

{kind=link}